In recent years, some banks in the United States have created what they call Islamic mortgage contracts in an attempt to attract Muslim customers. This leads some home buyers to wonder if an Islamic mortgage through a bank is a good alternative.

The answer is no — a bank in the U.S. is still a bank, and its products are problematic for customers trying to follow Islamic principles.

Shariah law strictly prohibits the practice of riba, which is the lending and borrowing of money at interest. The use of interest is at the heart of a U.S. bank’s business practice, and it is how they earn their income. Banks convert cash deposits into debt, selling more debt through credit cards or loans. Financing a home through a bank or subsidiary of a bank means supporting ventures prohibited by Islam.

Guidance Residential, on the other hand, is not a bank, and the income that we use to help purchase your home is earned in a halal manner. U.S. banking laws actually prevent banks from investing in and owning real property, making it impossible for them to become a co-owner and set up an LLC as Guidance Residential does.

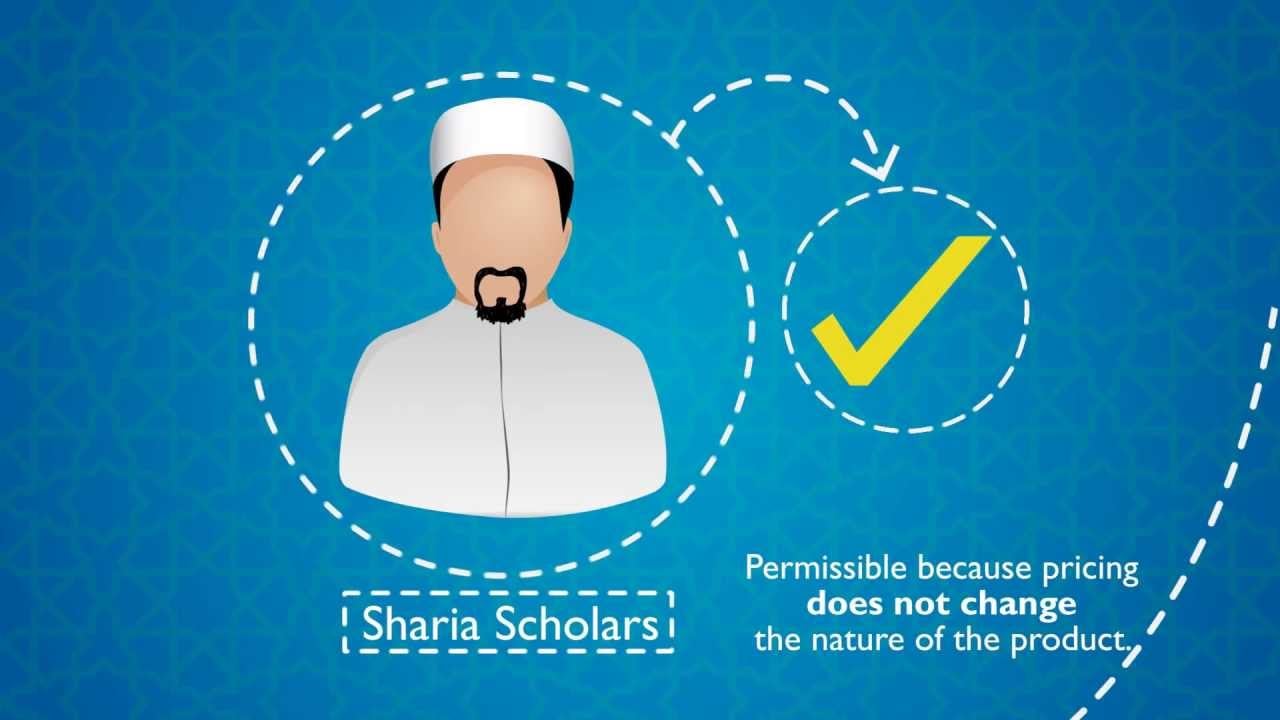

The esteemed Assembly of Muslim Jurists of America (AMJA) has passed a resolution naming Guidance Residential and our Declining Balance Co-ownership Program as a “permissible’’ path to Muslim Americans in need of home financing. The contract was found to be “sound in general.” Others who happened to be subsidiaries of banks were either regarded as companies that the Muslim public “is not allowed to deal with’’ or can deal with “only if one is in a state of dire need,’’ adding, “whoever remains away from them has kept himself safe and has protected his faith and honor.”

As a wholly-owned Muslim organization, Guidance Residential was structured as a financial services company — not as a bank nor a subsidiary of a bank.

Guidance Residential is the only non-bank and riba-free financing provider approved by an independent Shariah board, giving you the confidence that you can buy a home without compromising your values.

Watch this video to learn more about how Guidance is different from a bank and how an LLC makes all the difference.

.jpg)

.png?width=1200&length=1200&name=MASCON_Google%20Review%20Banner%20for%20Landing%20Page%20(1).png)